Download PDF

Download PDFConvexity, which measures interest rate sensitivity and drives the risk and return profiles of fixed income products, is an important concept that investors can utilize to boost total return and manage risk. It can be particularly important and may increase sharply during periods in which interest rates move quickly and with more volatility. We identified four areas of securitized products that offer interesting convexity anomalies or opportunities in the current rate environment.

Agency Mortgage-backed Securities (MBS)

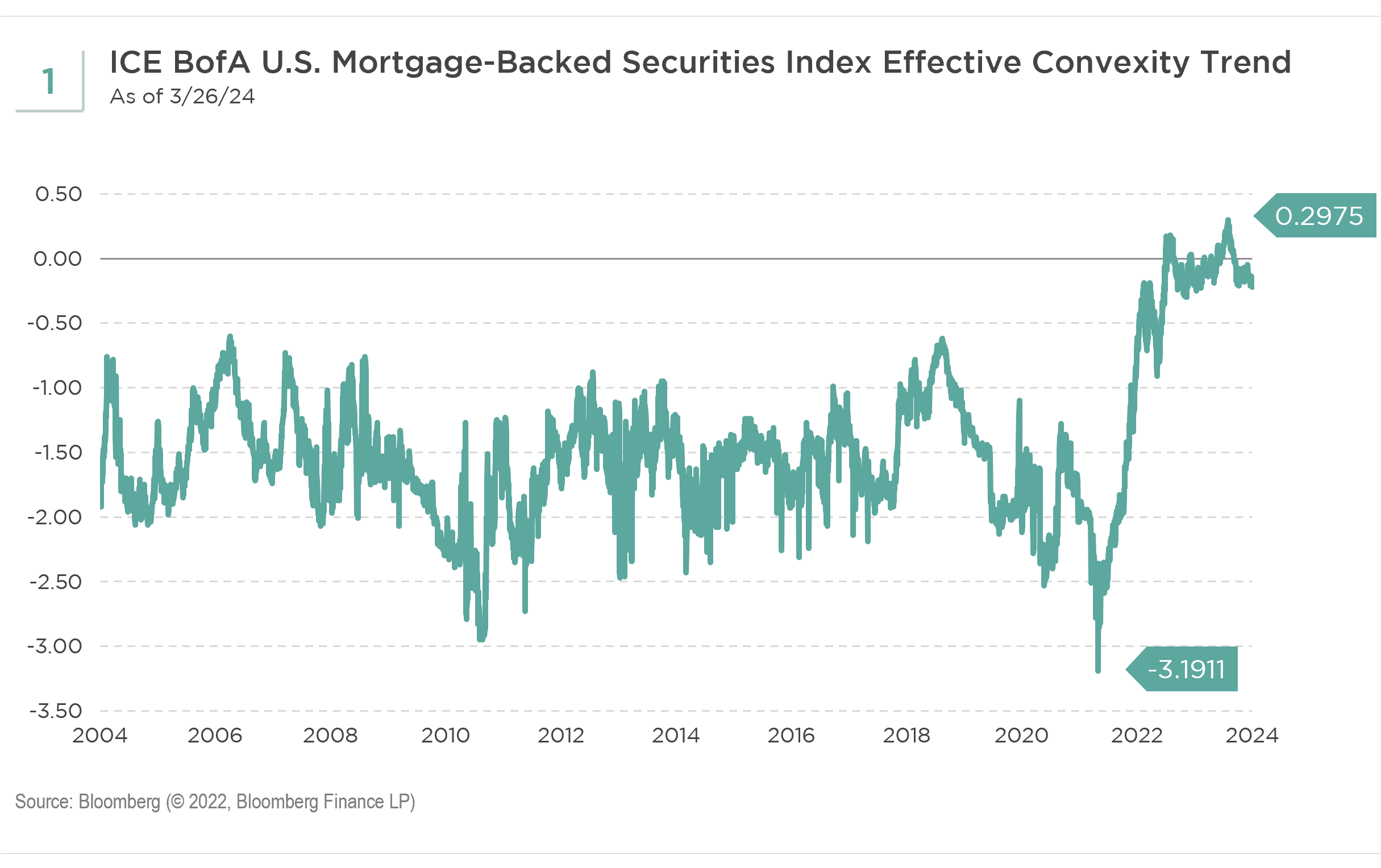

Opportunity: Agency MBS are well known for having negative convexity, due to the embedded prepayment option. However, unique market conditions have created an unusual anomaly. The Federal Reserve’s (Fed’s) steep interest rate hikes increased 30-year mortgage rates to over 7%, leaving more than 97% of existing mortgage holders locked in at low fixed mortgage rates and out of the money to refinance, according to Goldman Sachs research estimates.1 Furthermore, poor home affordability, lack of supply, and high mortgage rates decimated housing activities and effectively locked first-time home buyers out of the market. Therefore, the convexity of current coupon mortgages is the least negative for the first time in history, creating an unprecedented anomaly of the convexity profile (see Exhibit 1). In addition to cheap valuations, this unique situation further enhances the attractiveness of the asset class.

Risks: The market technical may be the main risk as the Fed continues to run off its MBS portfolio while banks have not yet returned to the market, waiting for more clarity on the regulatory front. Additionally, the convexity opportunity in MBS could reverse to negative territory in the case of a hard landing or severe recession, resulting in a fast and sharp rate rally by more than 200 basis points (bps) from current levels. In this scenario, however, agency MBS should hold up well as haven assets.

Credit Risk Transfers (CRT)

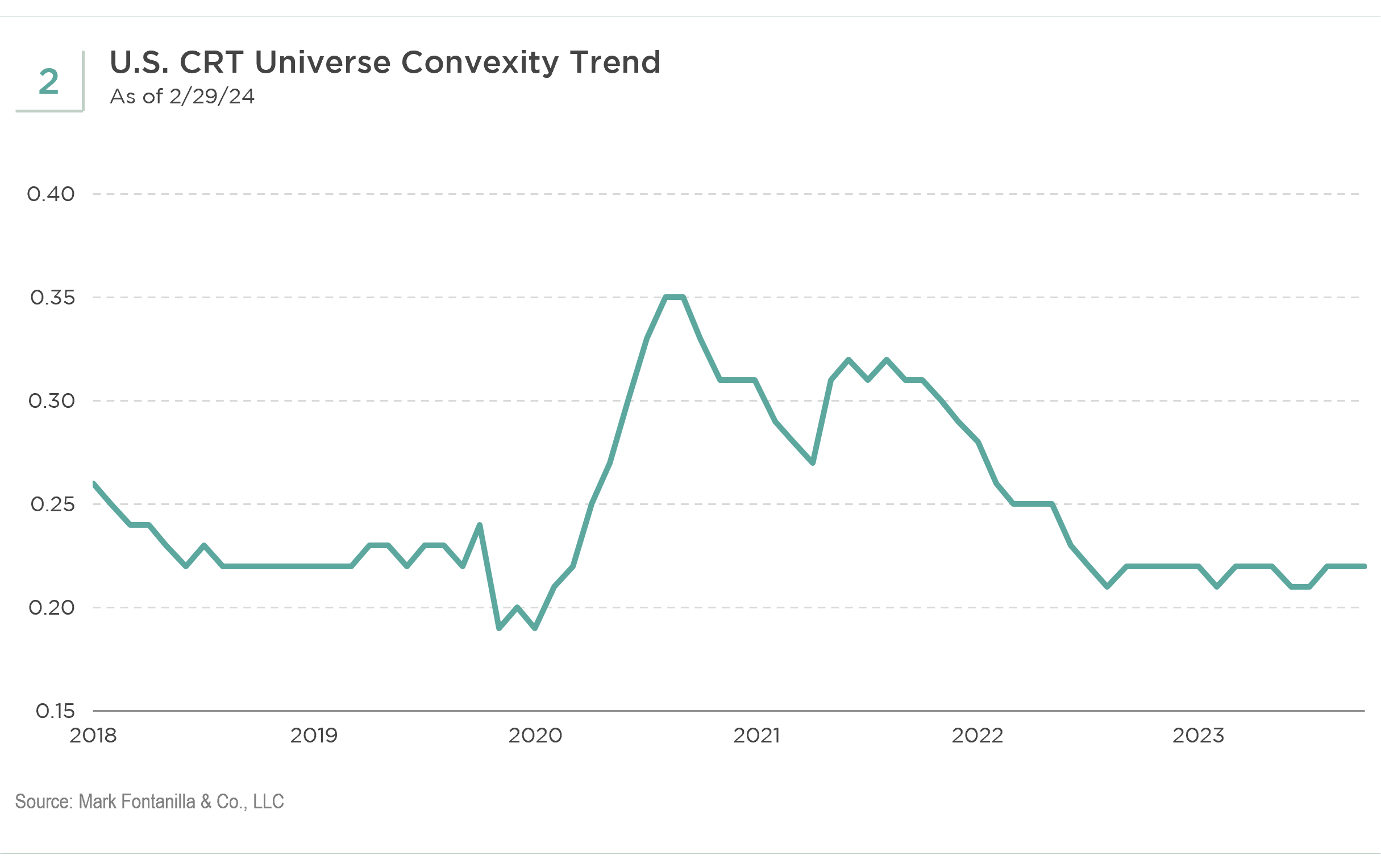

Opportunity: We like CRT subordinate bonds that compensate for the credit risk, with high floating rate coupons and premium price. These bonds are likely to see their average life extend and cumulative coupon payments increase due to slower prepayments when interest rates rise. We believe both mezzanine and subordinated tranches provide attractive all-in yields with low interest rate sensitivity due to low convexity. As investors seek to protect their portfolios from rising interest rates, CRT bonds can potentially serve as a great hedging tool.

- Floating rate coupon: CRTs are structured as uncapped floating rate bonds. Using the 30-day Secured Overnight Financing Rate (SOFR) as a benchmark, the floating rate coupons reset every month. Therefore, the convexity is low with short duration (see Exhibit 2). As interest rates rise, the floater coupon payments increase, reducing the bond’s price sensitivity to rate changes. In the meantime, higher coupon bonds that are at premium prices benefit from a rise in interest rates as slower prepayment activity increases the IO (interest only) value.

- Position in the capital stack: The deal structure waterfall of CRTs adds complexity to understanding the sensitivity to interest rates. Mezzanine bonds at the higher part of capital stack are the first to receive prepayments and the last to take losses from the underlying mortgage collateral. Mezzanine tranches are more susceptible to prepayment speed fluctuation, however, the more out-of-the-money the prepayment option is as a result of the “lock-in” and “lock-out” effect, the more muted the impact. Subordinated tranches, which are locked out from cashflow until mezzanine tranches are paid off, are more resilient to both prepayment risk and credit losses due to deal deleveraging, given the robust housing and job markets.

Risks: The risk of this investment is a hard landing or severe recession accompanied by a housing crisis in which the credit losses erode the credit supports of these bonds. We deem this scenario unlikely.

Non-agency Commercial Mortgage-backed Securities (CMBS)

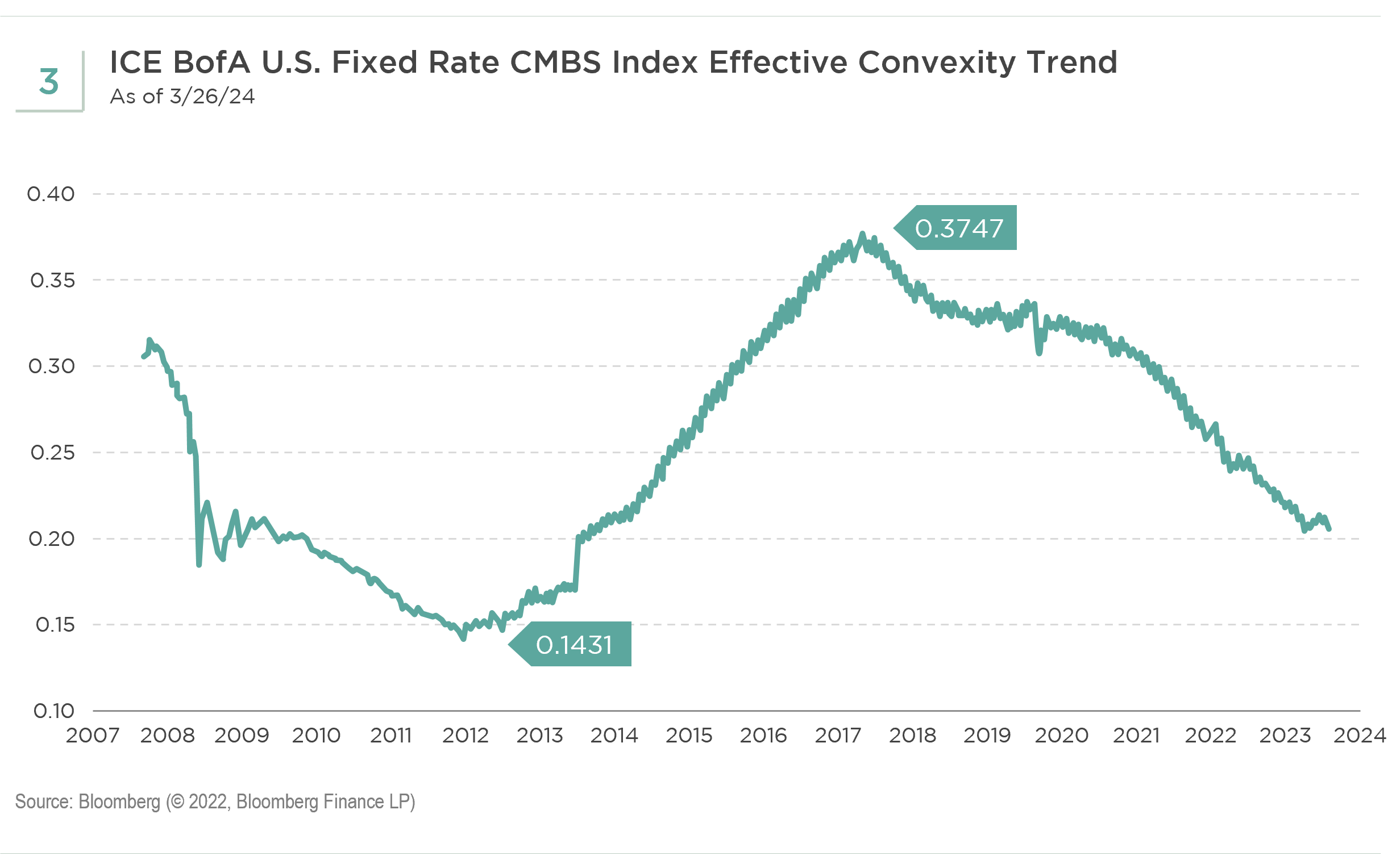

Opportunity: CMBS have been weathering a perfect storm of interest rate hikes and office property recession. The chart below shows the convexity of the ICE BofA CMBS Index has declined to a post-Global Financial Crisis (GFC) low (see Exhibit 3). The increasing inclusion of newer deals of 5-year maturity in lieu of the traditional 10-year maturity also has helped lower the convexity since 2020. In addition, lack of issuance has shortened the duration of the CMBS market. Since the GFC, conduit CMBS issuance peaked in 2015. Investment grade senior tranches of CMBS can exhibit positive convexity due to prepayment restrictions, including yield maintenance defeasance, prepayment penalties, and lockouts, while being protected from losses by credit support. We believe investment grade-rated CMBS look attractive while avoiding non-investment grade credit risk.

Risks: Should the Fed delay rate cuts and the office crisis deteriorate further, spreading to other property types and triggering credit losses in higher-quality investment grade CMBS bonds, this investment will not work. However, we believe most of the credit risk is priced in, and investment grade bonds are unlikely to take losses.

Subprime Auto Asset-backed Securities (ABS)

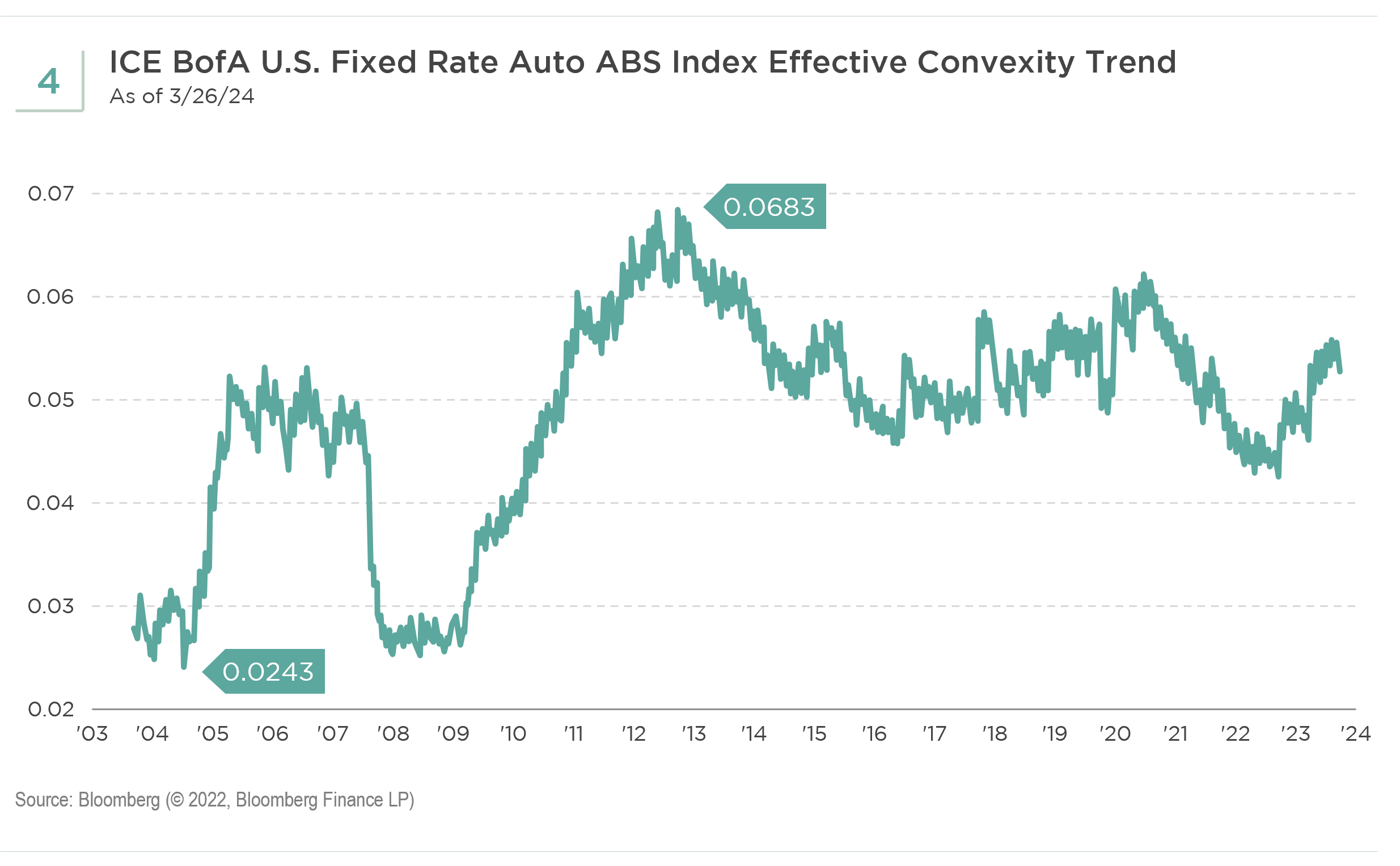

Opportunity: Subprime auto ABS may help offset overall portfolio interest rate sensitivity. Auto loans are less sensitive to interest rates than mortgages as the economics for borrowers to refinance are lower, due mainly to smaller loan balances and shorter loan terms. In addition, cars are depreciating assets, which makes them less attractive to refinance. Subprime auto ABS are known for their short duration structure and short term to maturity, and deal structures typically are designed to be sequential and fast deleveraging. Hence, subprime auto ABS convexity tends to be very moderate and flat. Exhibit 4 displays the convexity trend of auto ABS index, which is close to zero. With rates potentially staying higher for longer, investing in short-duration subprime auto ABS can reduce rate sensitivity.

Risks: If the job market worsens significantly along with a hard landing, subprime auto ABS bond defaults may increase sharply. However, we believe the potential credit losses should be absorbed by the cushion provided by credit enhancements and the fast deleveraging of the deal structure.

Conclusion

The convexity profiles of bonds are not static and can change based on market conditions. Currently, several securitized products are either moderately positively convex or the least negatively convex in history. These anomalies are due to the out-of-money nature of embedded options, uncapped floater coupon features, sequential structure of cashflow payments, or shorter maturity bond issuance. To potentially optimize return and manage risk through convexity, one must consider the outlook for interest rates. If investors are of the view that a big rate move is coming along with high rate volatility, then the case could be made for extending convexity by investing in high convexity bonds. Right now, MBS offers substantial nominal spread pickup over corporates, which presumably would compensate for at least part of the convexity differential. However, if investors have the view that rates will remain narrowly range-bound, and rate volatility will decline—our base case—we believe it makes sense to sell convexity or invest in low convexity, which is equivalent to buying MBS and low convexity products like CRT, non-agency CMBS, and subprime auto ABS.

1 Goldman Sachs Credit Strategy Research, "The Structured Credit Trader,” March 21, 2024.

Index Definitions:

ICE BofA U.S. Mortgage-Backed Securities Index tracks the performance of U.S. dollar-denominated, fixed-rate and hybrid residential mortgage pass-through securities publicly issued by U.S. Agencies in the domestic market. Included in the index are 30-year, 20-year, 15-year and interest-only, fixed-rate mortgage pools, provided they have at least one year remaining to final maturity and a minimum amount outstanding of at least $5 billion per generic coupon and $250 million per production year within each generic coupon.

ICE BofA U.S. Fixed Rate CMBS tracks the performance of U.S. dollar-denominated fixed-rate commercial mortgage-backed securities publicly issued in the U.S. domestic market.

ICE BofA U.S. Fixed Rate Auto Asset-Backed Securities Index tracks the performance of U.S. dollar-denominated, fixed-rate, investment grade (IG) auto loan asset-backed securities publicly issued in the U.S. domestic market.

Groupthink is bad, especially at investment management firms. Brandywine Global therefore takes special care to ensure our corporate culture and investment processes support the articulation of diverse viewpoints. This blog is no different. The opinions expressed by our bloggers may sometimes challenge active positioning within one or more of our strategies. Each blogger represents one market view amongst many expressed at Brandywine Global. Although individual opinions will differ, our investment process and macro outlook will remain driven by a team approach.